Lounge

May 7, 2015

Chapter 6: America's Negative Savings Rate and Japan's Uncomfortably Similar Situation

Chapter 6: America's Negative Savings Rate and Japan's Situation, Which Is Not an Unrelated Matter

Factors That Affect a Nation's Rise and Fall

By Shizuyuki Ima

Understanding the Differences in National Conditions Between Japan and the U.S.

Understanding the Differences in National Conditions Between Japan and the U.S.

Imagine a life with no savings and only debt. We would all be filled with anxiety and shudder.

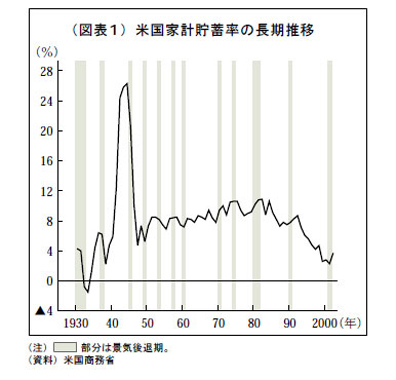

In fact, America's savings rate turned negative in 2005. A negative rate means not just zero savings, but a state of being in debt.

This is the first time the savings rate has turned negative since the unprecedented Great Depression triggered by the stock market crash of October 1929. To be precise, it's the first time in over 70 years, since the most severe years of the depression in 1932-33.

This is extremely important. In a nutshell, it signifies the entrenchment of what is often called 'excessive consumption'.

Let's consider a specific example. In America, it has become commonplace to easily borrow money by using the equity in one's home—that is, the value of the home exceeding the outstanding loan balance—as collateral. Financial institutions eagerly lend money using homes with outstanding mortgages as collateral. In other words, home equity loans have expanded, driving personal consumption. The situation is quite different from Japan.

A recent survey by the U.S. Federal Reserve Board (equivalent to Japan's Bank of Japan) shows that in 2004, households borrowed approximately $600 billion using their homes as collateral, which translates to a staggering 70 trillion yen. Essentially, it's a classic pattern of consuming by borrowing. This has become a source of volatility for the American economy.

To briefly explain the meaning of the savings rate as a review, it is the ratio of savings to disposable income (take-home pay).

For a salaried household, disposable income is what remains after deducting taxes such as income and resident taxes, as well as pension and health insurance premiums, from their earnings.

From this take-home pay, expenses for food, education, housing, etc., are paid, and the remainder becomes savings. Therefore, the savings rate (surplus rate) is calculated by dividing the amount of savings by disposable income (as a percentage).

What we must understand clearly here is that a savings rate of zero or negative has an impact that can affect a nation's rise and fall. Household savings are deposited in banks and post offices. Banks then lend this capital (savings) for corporate capital investment, individual home loans, and to finance government deficits.

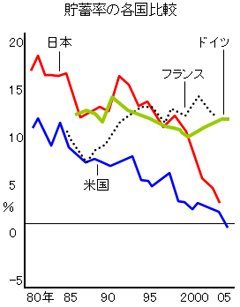

It goes without saying that it would be a serious problem if this capital, savings, became zero or negative. The highest average savings rate in post-war America was in the 9.0% range during the 1980s. Since then, it has steadily declined.

What about Japan? As of 2004, according to data compiled by the Cabinet Office, the savings rate was 2.8%, a low not seen in 55 years. While Japan boasted a high savings rate of around 20% in the 1980s, it has drastically changed. There are various reasons for this decline, but they can be summarized as the prolonged economic stagnation and the advent of an aging society.

Finally, it is essential to add that there are significant reasons why America, despite its negative savings rate of -0.4% (January-November 2004), remains at the pinnacle of the world in both political and economic spheres.

It is the world's leading industrial and technological power, a resource-rich nation, an agricultural powerhouse, and the world's largest military power. This is why the U.S. dollar reigns as the world's key currency. The U.S. dollar can purchase any goods needed worldwide and can be used anywhere, even at the ends of the earth. This signifies America's credibility itself.

America is a country with massive deficits in both its current account, particularly the trade balance, and its fiscal balance. Despite this, money continues to flow in from overseas because foreign countries still recognize it as a secure and trustworthy nation.

For example, countries are still competing to buy high-yield U.S. Treasury bonds. Recently, the U.S. Treasury conducted an auction for 30-year Treasury bonds, with a massive issuance of $14 billion (approximately 1.65 trillion yen). The bids received were 2.05 times the issuance amount. This is money (bonds) being used for the war efforts in Iraq and Afghanistan.

America is a completely different country from Japan, which lacks significant resources. Please keep in mind that the savings rate is of utmost importance for both households and the nation.

*GDP Per Capita Falls to 14th in the World; Savings Rate Hits Record Low - 2005 National Accounts

On the 12th, the Cabinet Office announced the 2005 National Accounts, which serve as a financial statement for the Japanese economy. When comparing nominal GDP per capita, converted to U.S. dollars, with other countries, Japan fell from 11th place in 2004 to 14th due to its relatively low growth rate and the impact of the strong euro.

While Japan maintained its position as the second-largest economy in terms of total GDP, trailing only the United States, it was surpassed by countries like Finland and Austria in per capita comparisons. Both of these countries use the euro, and the strong euro has inflated their dollar-denominated GDP.

Disposable income, which is household income minus taxes and social security contributions, increased by 0.7% from fiscal year 2004 to 290.3 trillion yen. On the other hand, the savings rate, which indicates the proportion of income saved, fell for the eighth consecutive year to 3.1%, a record low. This is likely due to increased consumption driven by rising incomes and stock prices, as well as a growing number of retirees drawing down their savings. (January 12, 2007)